STEFANO RIELA

Europe Institute, University of Auckland, New Zealand

Stupide. So much so that with Covid-19 the fiscal rules for the Economic and Monetary Union (EMU) of the EU have been suspended. After almost twenty years, that hardly institutional attribute expressed by one of the most institutional figures in the EU still echoes. The then President of the European Commission Romano Prodi had criticized, in an interview with Le Monde on 18 October 2002, the rigidity of the Stability and Growth Pact (hereinafter “the Pact”).

The Pact was based on two pillars: the carrot of Teutonic credibility on the monetary policy front and the stick that, starting from a minor lèse-majesté for a preventive control on public finance balances, could reach a less slight monetary sanction in case excessive deficit, the infamous 3% of GDP threshold. The objectivity of these rules, which in a Manichean manner divided fiscal policies into virtuous and vicious based on the annual balance, did not do justice to the quality of public spending. The fact is that a year later, the stupidity of the design of the Pact was translated downstream on its enforcement when, in November 2003, the Ecofin Council did not vote on the sanctions proposed by the Commission for France and Germany for excessive deficit[1].

However, the alarm bell had sounded, and in 2005 the Pact was reformed. But not in the direction hoped for by Prodi, namely that of separating expenditure on investments functional to growth – the so-called golden rule – from the calculation of the ‘bad’ deficit for the purposes of the Pact. The 2005 reform, on the other hand, gave more attention to the economic cycle by inviting countries to tighten fiscal policy in good times, and allowing more room for manoeuvre to ease it in difficult times. With this greater flexibility in the interpretation of the rules, the Pact seemed to work in the following two years until the financial crisis (except for Greece’s cooked books, but that’s another story).

In 2008, a further fragility was discovered in the EMU coordination system. A monomaniacal obsession with public balances had eclipsed other imbalances

including, for example, that on the private debt front. A policy of low rates in the euro area, consistent with average inflation, had inflated a bubble of contingent liabilities that exploded in countries such as Ireland and Spain. In reality, the crisis would also have hit other countries that had previously gone into debt disguised as Germans (when the word spread had not yet entered the common language) thinking of deceiving the markets by postponing the necessary structural reforms; markets that evidently did not believe in the cruelty of the ‘no bail-out’ clause put down in black and white in the Treaty[2] .

During the sovereign debt crisis, between 2011 and 2014, the Pact was affected by a sequence of reforms known in the jargon of cognoscenti ‘Six-Pack’, ‘Two-Pack’ and ‘Fiscal Compact’. Interesting is the one that aims to resolve what happened in the Council in November 2003, making the sanctions proposed by the Commission automatic without the need for the approval of the Council, which can only block them, by a qualified majority (the so-called reverse qualified majority voting, RQMV). But a more decisive procedure on enforcement has been accompanied by greater discretion with which tax policies are assessed by the Commission[3] .

On 3 March the European Commission, in the person of the Commissioner for the Economy Paolo Gentiloni, decided to extend the suspension of the Pact decided last year from 2021 to 2022[4]. This is to allow countries to counter the effects of the pandemic caused by Covid-19. This suspension is possible thanks to a safeguard clause that can be activated in times of severe economic recession to allow countries to temporarily move away from the path towards the values that symbolize a virtuous fiscal policy. According to data published by the Commission in February 2021[5], after the GDP contraction of 6.8% in 2020, the euro area is expected to grow by 3.8% in 2021 and 2022.

Will there be a return to the same Pact after Covid-19?

The Council will certainly approve the Commission’s proposal to keep the Pact frozen again until 2022. With the expected rebound in GDP, it would seem that in 2023 we could return to the status quo ante. Will we then return to the same Pact?

More than twenty years after the entry into force of the Pact, fiscal policy rules based on four different variables have accumulated: deficit, debt, expenditure and the balance of the structural budget. For the latter, the calculation of the level of GDP is required in a situation neither of economic boom nor of downturn, ie, when the output gap is zero[6]; since this situation is entirely theoretical and unobservable, different methodologies can be used as, for example, the European Commission, IMF and OECD do[7].

All this complexity takes shape in the vade mecum to the Pact that the Commission has published since 2013: the latest edition[8] consists of 108 pages in which it is clear that the original objectivity, however stupid (Prodi dixit), has been sacrificed on the altar of flexibility and negotiation between countries and the Commission. Proof? despite multiple violations, no country has ever paid any sanctions[9] (honestly, what’s the point of fining a country that already has budget problems?).

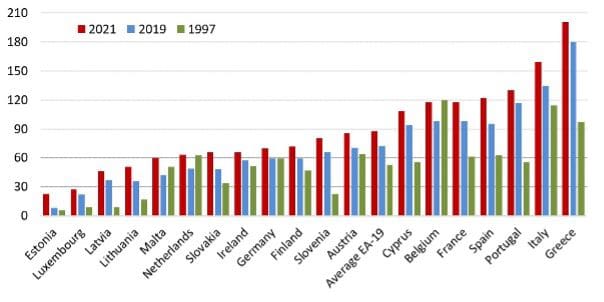

Source: European Commission – AMECO database

Even before Covid, the European Commission had launched, in February 2020, a public debate on the effectiveness of economic surveillance[10]. Now the picture has changed dramatically, just look at the jump in public debt: the average of the 19 euro area countries will move from 72.3% to 87.6% from 2019 to 2021.

Many countries are well above that 60% considered a sustainable level of public debt given other parameters which, at the time of the Maastricht Treaty, reflected realistic assumptions.

It is true that there is no clear-cut threshold above which a debt is in itself unsustainable; but it is also true that the days of ‘German-style’ public debt financing rates are over. After the financial crisis, the spreads of many heavily indebted countries have remained positive and interest spending subtracts resources that could be invested to sustain competitiveness. The investment trend in the euro area was already waning[11] : the average in the 19 members had gone from 24% of GDP in the decade 1999-2008, to 20% in the decade 2010-2019. And Covid-19 risks reducing them further.

Surely the so-called “Recovery and Resilience Facility” will help support the implementation of reforms and investments with € 312.5 billion in grants and up to € 360 billion in loans. However, this new European debt instrument is temporary and any reform of the Pact cannot derogate from two fundamental rules: mathematics and politics.

The fiscal policy of a country is subject to an intertemporal budget constraint: deficits must be offset by surpluses in such a way that their sum, taking into account the value of time, is zero; if this were not the case, debt would explode in the long run and no one would be willing to finance a country with such risk.

In the EU, but also in other contexts, financial assistance, as well as forms of debt mutualisation, comes at conditions that, for the lovers of national sovereignty, can be a significant cost. After all, there is no such thing as a free meal.

[1] Judgment of the Court of Justice of 13 July 2004.

[2] The Court of Justice has ruled that the no bail-out clause prohibits member countries from granting financial assistance to a country if this would reduce its incentive to conduct a sound budgetary policy. However, if financial assistance in favour of a country is instead aimed at safeguarding the stability of the euro area as a whole, and is subject to conditions as in the case of the European Stability Mechanism, then it does not violate the Treaty (judgment of 27 November 2012 relating to Pringle case C-370/12).

[3] See for example art. 2 par. 3 of the EC Council Regulation 1467/97 of 7 July 1997 modified in 2011 by the EU Council Regulation 1177/2011.

[4] On 23 March 2020, the Ecofin Council approved the Commission Communication of 20 March 2020 on the activation of the general safeguard clause of the Stability and Growth Pact COM (2020) 123.

[5] European Commission, “European Economic Forecast – Winter 2021”, European Economy Institutional Paper 144 (2021) (link).

[6] Output gap is the difference between the actual Gross Domestic Product (GDP) of a country and its potential GDP as a percentage of potential GDP. The potential GDP is what a country can produce when unemployment is at its natural rate and there is no inflationary pressure. Unlike actual GDP, potential GDP is not observable but must be estimated.

[7] European Parliament, “Potential output estimates and their role in the EU fiscal policy surveillance” Economic Governance Support Unit (EGOV), Directorate-General for Internal Policies, PE 547.407, February 2020 (link).

[8] European Commission, “Vade Mecum on Stability and Growth Pact”, European Economy Institutional Paper 101 (2019) (link).

[9] See Chapter 3 of “When and How to Deactivate the SGP General Escape Clause? Fiscal Surveillance after the Break”, European Parliament, Economic Governance Support Unit (EGOV), DirectorateGeneral for Internal Policies, PE 651.376, December 2020 (link).

[10] European Commission, “Review of economic governance”, COM (2020) 55 of 5 February 2020.

[11] We use “Gross fixed capital formation” defined as acquisitions of resident producers, minus disposals, of tangible and intangible assets. This applies in particular to machinery, equipment, vehicles, homes and other buildings.

Created and maintained by ScorpioTek